The Complete Multi-Board 8.0 Guide: Every Clause of the Illinois Real Estate Contract Explained

If you're buying or selling a home in Illinois, you're almost certainly signing a Multi-Board Residential Real Estate Contract. Version 8.0 dropped in February 2025, and it's the most significant update in years. This guide walks through all 38 paragraphs.

Just need the contract?

Download the Multi-Board 8.0 Residential Real Estate Contract and get started.

Download Multi-Board 8.0 Contract (PDF)

What Is the Multi-Board Contract?

The Multi-Board Residential Real Estate Contract is the standard purchase agreement for residential real estate transactions across metropolitan Chicago and most of Illinois. It's approved by over 20 REALTOR associations and bar associations, including the Chicago Association of REALTORS, the Illinois Real Estate Lawyers Association, and bar associations from Cook County to Will County.

If your agent hands you a contract for a house, condo, or townhome in Illinois, this is almost certainly the form you're signing.

What Changed from 7.0 to 8.0?

The headline change is Paragraph 4, a brand-new section on buyer brokerage compensation driven by the NAR settlement. Under the old rules, the seller's listing agreement typically covered both agents' commissions. Now, buyer brokerage compensation must be addressed separately.

Other notable changes in 8.0:

- Paragraph 13(d): A new "non-counteroffer proposal" mechanism that lets attorneys make proposals that don't kill the contract if rejected

- Updated fixtures checklist: Electric vehicle charging systems, video doorbells, and surveillance systems added

- Clarified financing alternatives: The three-tier financing structure (contingency, cash-no-financing, cash-financing-allowed) is more clearly delineated

- Copyright date: 2025 Multi-Board Joint Venture

Let's go paragraph by paragraph.

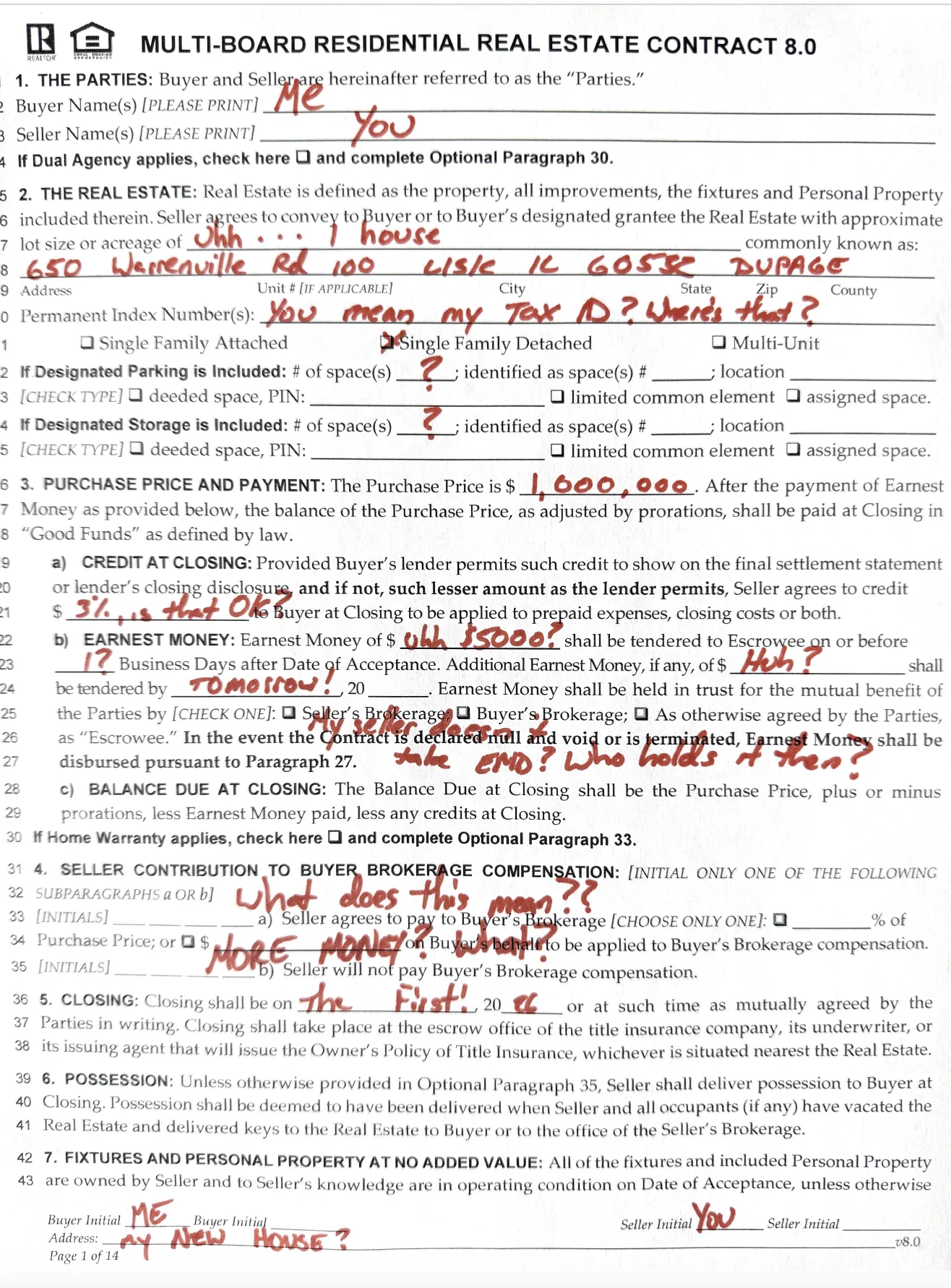

Paragraphs 1-2: The Parties and the Property

Paragraph 1 identifies the buyer and seller. Simple enough, but watch for trusts, LLCs, and estate situations where the wrong entity name can torpedo a closing.

Paragraph 2 defines the "Real Estate," the property itself, all improvements, fixtures, and personal property included in the sale. You'll specify the address, PIN, property type (single family attached, detached, or multi-unit), and any designated parking or storage spaces.

The checkbox for dual agency (referencing Optional Paragraph 30) is right here at the top. If the same brokerage represents both sides, this must be initialed.

Attorney tip: Always verify the PIN against the legal description on the title commitment. Mismatches happen more often than you'd think.

Paragraph 3: Purchase Price and Payment

This paragraph does three things:

3(a): Credit at Closing

The seller can agree to credit the buyer a dollar amount toward prepaid expenses, closing costs, or both. The critical language new in 8.0: "and if not, such lesser amount as the lender permits." This means if the lender caps seller credits at 3% and the contract says $15,000, the credit automatically reduces to whatever the lender allows. No amendment needed.

3(b): Earnest Money

The deposit that shows the buyer is serious. Typically $5,000-$10,000 in the Chicago market, though it varies. Earnest money is held in trust by the escrowee (usually the seller's brokerage) and applied to the purchase price at closing.

The bolded language is crucial: "In the event the Contract is declared null and void or is terminated, Earnest Money shall be disbursed pursuant to Paragraph 27." This means every termination provision in the contract funnels back to Paragraph 27's disbursement mechanics.

3(c): Balance Due at Closing

Purchase price, plus or minus prorations, minus earnest money, minus credits. Paid in "Good Funds," which means wire transfer or cashier's check.

Attorney tip: The earnest money deadline is a real deadline. Under Illinois case law, if the buyer fails to deposit earnest money timely, the seller may have grounds to argue no binding contract was formed. See Catholic Charities v. Thorpe, 396 Ill.App.3d 77 (2009).

Paragraph 4: Seller Contribution to Buyer Brokerage Compensation (NEW)

This is the NAR settlement paragraph. One of two subparagraphs must be initialed:

(a) Seller agrees to pay a percentage of the purchase price OR a flat dollar amount toward the buyer's brokerage compensation.

(b) Seller will not pay buyer brokerage compensation.

This is the biggest structural change from 7.0. Previously, the listing agreement handled agent compensation on both sides. Now it's explicitly addressed in the purchase contract. If you're a buyer's attorney, make sure your client understands how their agent is getting paid before they sign.