Illinois Short Sale Guide 2026: What Every Homeowner Needs to Know

If you are behind on your mortgage in Illinois, you have more options than you think. This guide explains all of them, in plain language, with an FHA payoff calculator built in.

What is a Short Sale in a Real Estate Context?

A short sale is a lifeline for homeowners underwater on their mortgage, allowing them to sell their property for less than the remaining mortgage balance. It's a viable alternative to foreclosure, especially for those under financial strain. In the state of Illinois, short sales come with their own set of guidelines and requirements that homeowners and buyers must adhere to. As mortgage foreclosure and short sale practitioners, we educate people on how to get through these tough times, without a tough time.

There are other solutions too, but those have their own article.

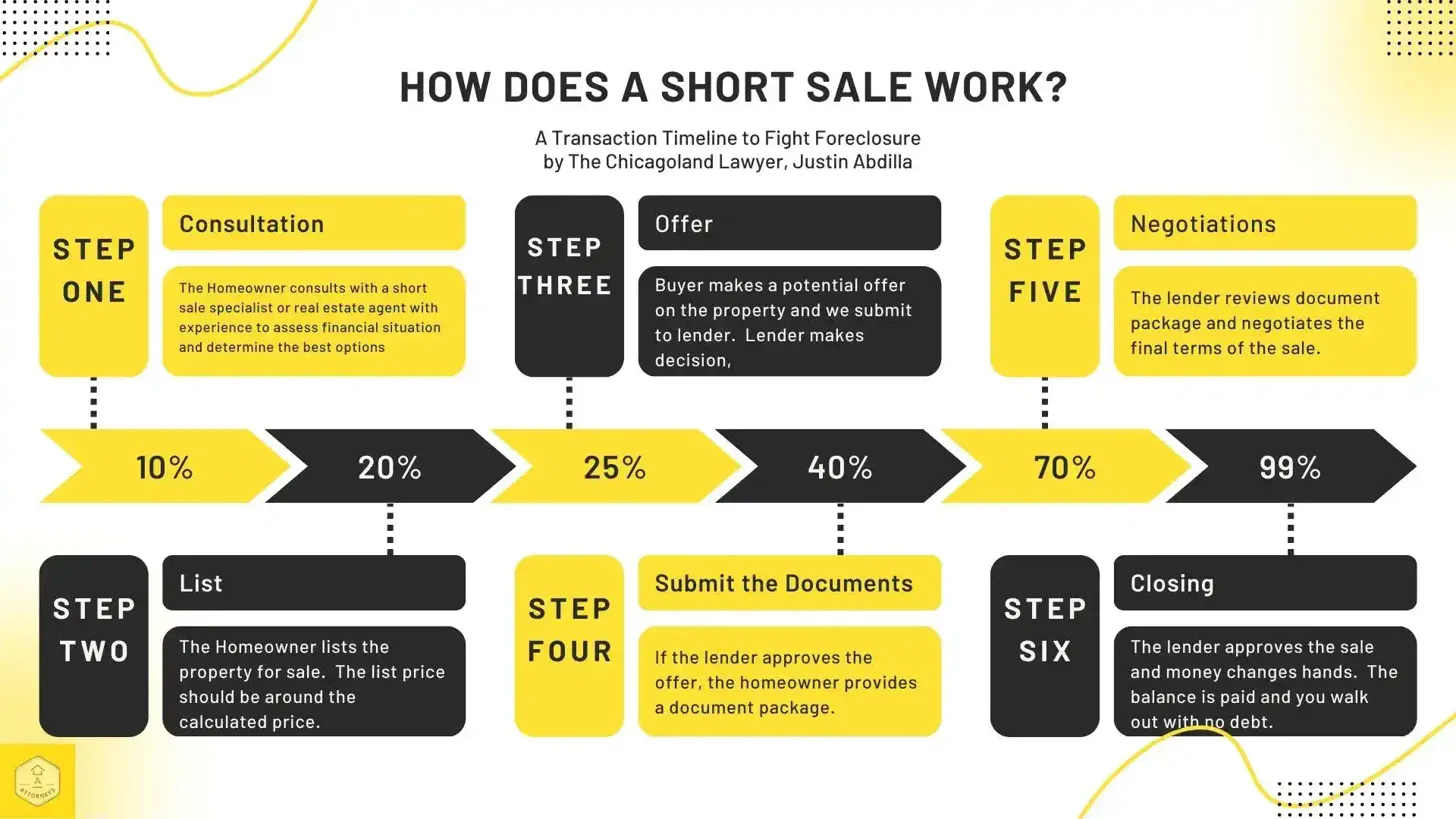

How Can I Short Sell My Home?

A short sale, simply put, is selling your property for less than what's left on your mortgage, with your lender's consent. Here are the six steps:

We often start for $0. The most we ever charge to begin is $300. You do not need money in hand to get legal help.

- Consult with a short sale specialist or real estate agent to determine if a short sale is the best option for you.

- List your property for sale at a lower price than the outstanding mortgage balance (use the calculator in this article).

- Once you get a good offer, forward it to your lender for their approval.

- If the offer gets the green light, prepare a short sale package. This includes your financial statements and a hardship letter to present to the lender.

- Negotiate the terms of the sale with the lender.

- Once the lender gives their approval, close the deal. Use the proceeds from the sale to settle your outstanding mortgage balance and gain freedom from any further debt repayment obligations.

The path to short selling isn't always smooth. It can be complicated, time-consuming, and not every lender is open to it. A short sale could also affect your credit score and may come with tax implications. More on that below, because the tax landscape changed significantly at the start of 2026.

Illinois Short Sale Procedures and FHA Calculator

Short sales are often the best strategic move to begin your financial recovery. If you're looking at foreclosure, your departure from your home should happen on your terms. Opting for a short sale of your property 'as is' is a common choice among sellers.

The first step in our collaboration involves an evaluation of your eligibility. Should we find your property aligns with our requirements, we'll move forward by presenting an offer to your bank as part of a comprehensive package, covering documents related to your financial status, hardship, and the short sale offer.

Essential Tool: The FHA Short Sale Payoff Calculator

A short sale payoff calculator is an invaluable tool for homeowners considering a short sale in Illinois. This calculator helps determine the potential proceeds from a short sale, taking into account factors such as the outstanding mortgage balance, closing costs, and any additional fees. By using this tool, homeowners can better understand the financial implications of a short sale and make informed decisions on how much to sell their house for.

FHA requires lenders to net at least 88% of the appraised value. Enter your numbers below to see if a short sale is viable for your situation.

This calculator provides estimates only. Actual FHA short sale approval depends on your specific lender, servicer guidelines, and current appraised value. Call for a free evaluation of your specific situation.

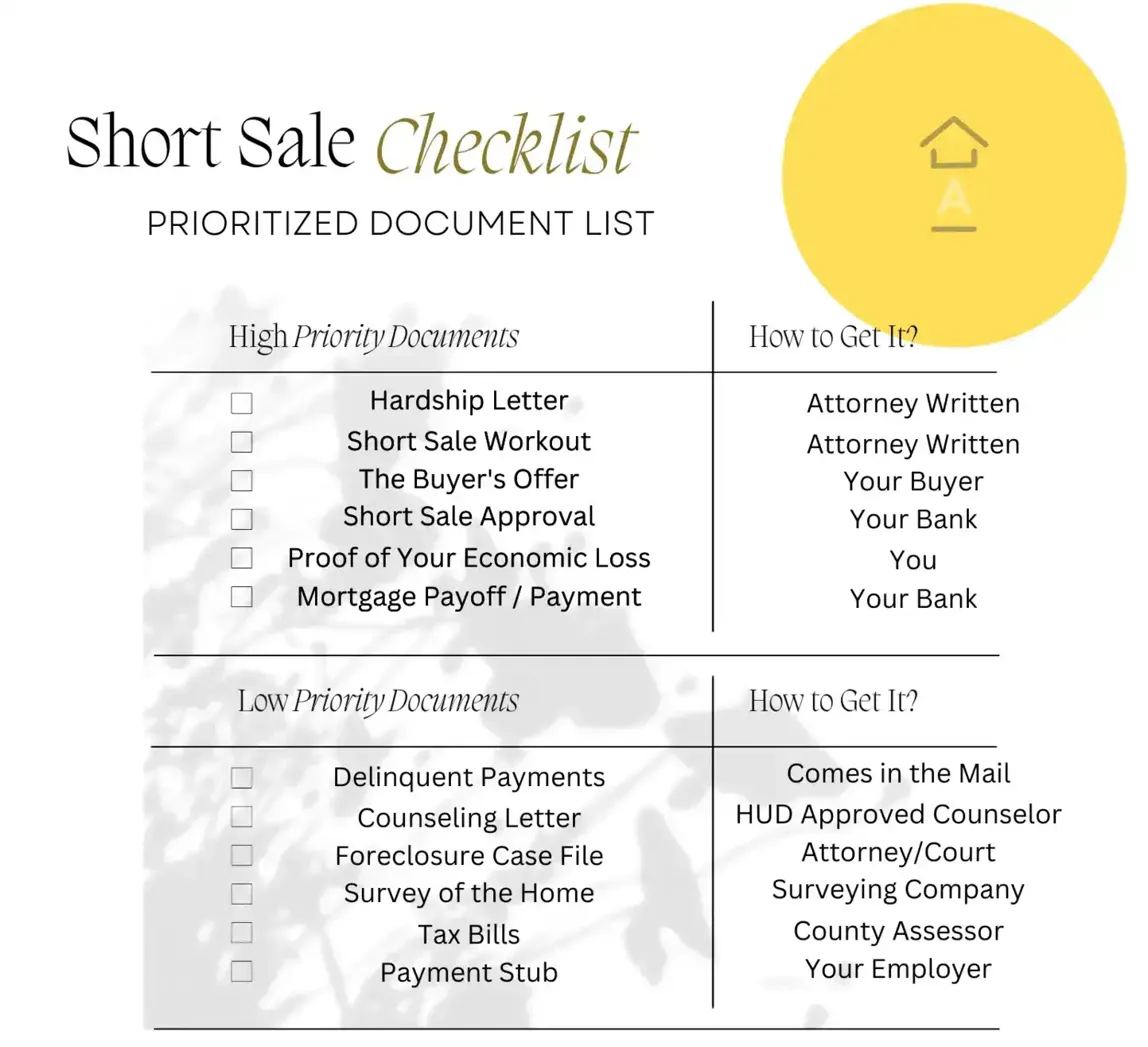

Which Documents Do I Need?

- A complete short sale package comprising your hardship letter, short sale offer, and other relevant items.

- Evidence indicating the date you fell behind on payments or missed one (if applicable).

- Our short sale offer, showing the amount the buyer is willing to pay for your property.

- Evidence of hardship illustrating why you cannot keep up with the house payments.

- Any documents associated with your short sale dealings with other entities, for instance, a short sale approval letter from a previous lender or divorce documents if relevant.

- Your most recent mortgage statement.

Illinois Short Sale Approval Process

Securing approval for a short sale isn't quick. You cannot cut corners; bank approval is a must. This approval stage might drag on for months, sometimes stretching beyond a year. The basis of short sale approval is your financial hardship as presented to the bank. It isn't about the equity in your home or its condition (unless you're trying to short sell a secondary property, like an investment property). Banks hold the final say on what they accept or reject. Our role is to ensure your documents present your case in the best possible light.

What if I Probably Could Afford the House or Want to Redeem it?

If the seller has money in the bank, including retirement funds, it is unlikely the lender will let the debt slide. The proof of income and assets must include income tax and bank statements going back at least two years. Sometimes sellers are unwilling to produce these documents because they conflict with information on the original loan application. If that's the case, the deal is unlikely to close.

How Does a Short Sale Work When HOA Fees and Taxes Are Owed

Dipping into the realm of short sales during foreclosure proceedings subjects your property to pre-foreclosure laws. Covering any outstanding charges or taxes is a prerequisite for moving forward. These dues might come as a surprise during our title search. Walking you through the process, we offer guidance to alleviate your financial stress.

Be vigilant in identifying all property liens, as they can multiply. The IRS has shown leniency toward federal tax liens since late 2008, permitting property sales without full repayment. Back taxes, though, persist after a short sale. Resolving a single mortgage lien is a simpler task.

What About Deficiency Judgments?

How Much Will It Cost?

In Illinois, short sale sellers are not required to pay upfront attorney fees. This makes it easier for financially struggling homeowners to access legal representation throughout the process. We often take clients with as little as $0 money down. The most we ever charge for short sale help is $300.00 down. We can also stop the foreclosure by making sure the judge knows what you're trying to do to save your house and responding to court obligations in a timely way.

2026 Foreclosure and Short Sale Estimates

Percentage of housing units with a foreclosure filing. Illinois tied for highest in the nation.

Illinois is one of the worst states in the country to fall behind on a mortgage. In the first half of 2025, ATTOM data showed Illinois tied with Delaware for the highest foreclosure rate in the nation, with 0.23% of housing units carrying a foreclosure filing. That is nearly double the national average of 0.13%. Illinois recorded 7,922 foreclosure starts in H1 2025 alone, and Chicago led all U.S. metropolitan areas in Q1 2025 with 3,789 foreclosure starts. Nationally, total foreclosure filings in H1 2025 reached 187,659 properties, up 5.8% from the same period in 2024. The trend is moving in the wrong direction for homeowners who are behind on payments.

As a foreclosure and short sale attorney, I want to frame this with risk and reward. Although each lender is different, every lender I've dealt with has a program to help. The inventory of short sale homes is still relatively low compared to historical highs, which means your home will sell if priced accordingly. Already in 2026, we have helped people in Aurora, Wheaton, Chicago, Dolton, Glen Ellyn, and Buffalo Grove sell homes in foreclosure.

On the typical short sale, the lender knows you have to hire professionals and pay your bills. They will, nearly without exception, leave you money for your closing professionals. So, you will likely have 6% of the purchase price (in this case 6% of the LTV) set aside for commissions and a small stipend for your closing attorney and title. Everybody can work together and you won't need to worry about coming out of pocket to pay your teammates.

Some sellers also receive cash at closing to help cover moving expenses. If your loan qualifies under the federal Home Affordable Foreclosure Alternatives program (HAFA), you may be eligible for relocation assistance. The exact amount depends on your lender and the terms of the program. When I evaluate your situation, I will tell you specifically what your lender offers and whether we can pursue it for you.

Free Consultation. Same-Day Response.

No obligation, no sales pitch. Tell me about your situation and I'll tell you what your options are.

Title Issues in Short Sale Transactions

Let's face it: in a short sale, the hardest obstacle to completing the transaction is the bank. You, the homeowner, will not have full control over the offer sheet or the final contract. The lender is just as much your Realtor's client as you are. The lender must approve the final closing statement and give you permission to close the sale.

The best thing to do is hire a firm with great knowledge of processing these transactions. A number of great Realtors in the Chicagoland area do amazing work with short sales.

When you accept an offer, the bank orders what is called a Broker Price Opinion, or BPO. A BPO is a quick market valuation performed by a real estate agent the bank hires to estimate what your home is worth. If the offer you accepted comes in lower than the BPO, the bank may reject the deal or counter at a higher price. Your team can challenge the BPO if it's inflated, which is more common than you'd think. Banks routinely overestimate value on distressed properties. That challenge is one of the most valuable things a good short sale attorney and Realtor can do for you.

Your professional team, hopefully including me, can work with the bank to get a better short sale appraisal and sell the home closer to its true value.

How We Calculate if We Can Help You

Banks have a clear bottom line before they let the debt go free. Normally this number is between 84% and 88% of your outstanding debt against the value of the home. LTV is the percentage of the mortgage loan debt divided by the appraisal amount. So if the bank is willing to reduce debt to 88%, that helps dramatically in keeping your LTV solid. If we can simultaneously challenge the appraisal amount, that also cuts the number. Our big goal is to get LTV under 90% if at all possible.

How Do I Buy a Short Sale Property?

Buying short sale homes in Illinois involves several crucial steps:

- Lender Approval: The lender must consent to the short sale since the home will sell for less than the outstanding loan balance. The lender's approval is a crucial part of the process.

- Seller's Hardship Demonstration: The seller must provide evidence of financial hardship. Lenders are more inclined to agree to a short sale when they understand the seller's financial difficulties and wish to avoid the foreclosure process.

- Home Pricing in Line with Market Value: Short sales often occur when property values have declined. The buyer's offer should typically reflect the current market value of the home.

- Disclosure of Short Sales: When a property is listed for less than the outstanding mortgage balance, this must be disclosed upfront. Potential buyers need to know that the sale price is lower than the mortgage balance, which means they will be negotiating with both the lender and the seller.

Steps to Buying a Short Sale Property

Step 1: Identifying Potential Short Sales

Search for pre-foreclosures in your area through online listings, courthouse records, legal ads, or by working with an experienced buyer's agent. Assess the outstanding loan balance relative to the property's approximate value to identify good candidates.

Step 2: Property Viewing

Properties needing work often sell below market, creating opportunity for investors and owner-occupants alike.

Evaluate the property's condition and estimate repair or renovation costs. Properties needing work may deter conventional buyers, increasing your chances of a successful short sale. There is a good chance you'll be the only bid.

Step 3: Conducting Research

Determine the property's value and profit potential, especially if you're an investor or a homeowner planning to live there. The Illinois flip market has remained active, and distressed properties often sell below what comparable renovated homes fetch. Do your due diligence on comparable sales before you make an offer.

Step 4: Discover All Liens and Mortgages

Inquire about liens on the property and identify the primary lien holder. Verify this information with a title search to ensure no undisclosed liens exist. We do those title searches through Citywide Title Agency or Chicago Title.

Step 5: Arrange Financing

Establish how you'll finance the property. If you have good credit, the existing lender may offer a loan, potentially expediting the application process. Prepare to move quickly, as lenders often require closing within 20 days of an agreement.

Step 6: Contact the Seller's Lender and Complete the Application

You or your agent should communicate with the lender's loss mitigation or resource recovery department. Obtain the homeowner's authorization for the lender to discuss the mortgage situation with you. Sometimes these take the form of nominee agreements.

Step 7: Prepare the Proposal

Assemble a package including the application, authorization letter, purchase and sale contract, hardship letter, property value statement, cost and liability details, and settlement statement.

Buying a Short Sale vs. Foreclosure Sale

A short sale is a voluntary sale by the homeowner, whereas a foreclosure is an involuntary sale initiated by the lender. In a short sale, the homeowner is still in possession of the property and working with the lender to sell for less than the outstanding mortgage balance. In a foreclosure, the lender has already taken possession and is selling to recoup their losses.

The short sale process is typically more complex and time-consuming than the foreclosure process. Short sales involve negotiations between the homeowner, the lender, and any other lien holders. In contrast, foreclosures are typically faster and more direct, with the lender taking ownership and selling at auction.

Short sale homes are often still occupied by the homeowner and may be better maintained than foreclosed homes, which may have been abandoned and left in disrepair.

Qualifying Hardships and the 129 Affidavit

When you apply for a short sale, the first step is to inform the bank why you got behind. Normally, your processor takes care of writing this letter for you. We make it as sympathetic as possible to appeal to the limited humanity in the lending industry. We tell your story about why you need a second chance.

The best qualifying hardships, in our experience, include:

- Loss of your job.

- Death or medical disability of yourself or a close family member.

- Reduction in work hours.

- Change in your usual salary.

- Transfer from your old job to somewhere new.

- Divorce or marital separation.

- A change in the interest rate on your loan, if the loan was adjustable.

- Being called to military service.

- Damage caused to your property or your livelihood by natural disaster.

Economic hardship takes many forms. If you've had a major life disruption that changed your ability to pay, we want to hear about it. Call us and let us hear your situation.

We often start for $0. The most we ever charge to begin is $300.

Illinois Foreclosure and Short Sale Timeline

Day 1 to 46: Your Missed Payment and Preforeclosure

When you first miss your payment, not much really changes in your day-to-day housing. The bank sends you a notice that they saw you missed your payment. Maybe they even let you go a month or two without sending anything particularly nasty. But sooner or later, the bank sends you a Grace Period Notice and tells you the past-due balance has to be paid right now. Then they send you a Notice of Intent to Accelerate, telling you that the hundreds of thousands of dollars you borrowed are due in 30 days. This is terrifying. What can you do?

It's at this stage that short sales have the greatest amount of success. Our team can help you work with your bank before the property gets to a foreclosure courtroom. This accomplishes two things. First, the bank will have fewer fees it can charge to you for the attorneys working your case. And second, the bank will be more willing to work on your proactive timeline instead of on the court's schedule. This is the best time to call an attorney and work something out with your lender.

Day 47 to 90: Foreclosure Complaint and Lis Pendens

In Illinois, your foreclosure court case will last a minimum of 7 months, giving you time to sell the property. We do not recommend waiting out that timeline. When the bank files your foreclosure complaint, they also file a Notice of Lis Pendens. You won't get that document in the mail, but it is vital to the short sale process. The Lis Pendens is a notice to prospective purchasers that you cannot sell the property right now. Nobody would ever miss a Lis Pendens, and it basically destroys whatever chance you had of selling your home conventionally. That's why it's critical to start as soon as possible.

Further, when you get a foreclosure complaint, the court in Illinois is putting the responsibility on you to act. Many homeowners do not know this, but if you receive a foreclosure complaint and you want more time, you must appear in court and respond. Illinois law (735 ILCS 5/15-1504 and 1506) allows the bank to take shortcuts in foreclosing if you do not respond to the complaint. They don't even have to show your non-payment if you don't respond. Act quickly and appropriately if the sheriff ever gives you a complaint.

Letting foreclosure run to completion often leaves the home vacant and deteriorating. A short sale gives you control over the exit.

After Day 210: Judgment

After your three missed payments, and after the Notice of Default and after you receive the complaint, you may face a foreclosure judgment. Don't panic.

In Illinois, foreclosure judgments do not end your rights in your home. We are perhaps the only state in America where that is true. Once you have a foreclosure judgment against you, the bank still cannot do anything to you for at least 90 days. This is the Homeowner's Right of Redemption. During this time, you can pay off your loan to remove the foreclosure. How might you do that? With a short sale. Sell the asset for an agreed-upon amount to pay off the foreclosure and vacate the judgment.

During this time, you will have a minimum of 42 days left to sell the home. It is possible to get extensions if you appear in court and properly ask the judge for one. At this stage, the bank typically wants to see 84% LTV of the property paid in the sale. The bank will not make it easy. If you are post-judgment in a foreclosure proceeding, you will need a good team on your side.

Too Late: Sheriff's Sale

We often start for $0. The most we ever charge to begin is $300.

What Happened to the Tax Break? The 2026 QPRI Update

This is the section I wish I didn't have to write, but you need to know about it before you make any decisions.

For years, there was a federal tax protection called the Qualified Principal Residence Indebtedness (QPRI) exclusion. Under that law, if your lender forgave $50,000 in mortgage debt as part of a short sale, you didn't have to pay income tax on that $50,000. Congress kept extending it. It helped a lot of people get through short sales without a surprise tax bill on top of everything else.

What this means practically: if your lender forgives debt as part of a short sale completed in 2026 or later, the IRS may treat that forgiven amount as ordinary income. Depending on what was forgiven and your tax bracket, that can be a significant number.

There is some good news. If you entered into a written short sale agreement before January 1, 2026, you may still qualify for the exclusion even if the closing happens later. And there are other tax protections that may apply: insolvency, bankruptcy discharge, and a few others. I'm an attorney, not a CPA, and the tax implications in your specific case depend on your numbers. What I can tell you is that before you close a short sale in 2026, you need a tax professional to look at the forgiven debt and tell you what you're facing.

This doesn't mean short sales are a bad idea. In most cases, a short sale is still far better than foreclosure, both for your credit and your ability to buy again. But the tax question is now a real part of the conversation in a way it wasn't a few years ago. Call me and I'll make sure you go in with your eyes open.

Frequently Asked Questions About Illinois Short Sales

How Will a Short Sale Affect My Credit

A short sale is a fantastic way to preserve your credit after foreclosure. Of course, if you're losing a home, your credit score will take a substantial hit. But you can minimize the credit hit's impact and duration if you deal with the problem proactively and responsibly. A short sale is your absolute best choice in nearly all circumstances.

How Long Will a Short Sale Affect My Credit?

This chart is optimistic. It assumes there are no other credit failings on your behalf once you get out of your foreclosure. For obvious reasons, that circumstance is unlikely, as many homeowners going through foreclosure are struggling due to an unmanageable hardship. But we can help you minimize your credit hit. With careful credit repair advice, we can help you shorten the duration of the report to just a few years.

Official Guidelines

Fannie Mae states that some borrowers with short sales and deed-in-lieu can qualify for a new loan in just two years, assuming no other defaults. Fannie Mae keeps foreclosures on your credit report for 7 years if you do nothing. If you have had a foreclosure before and are reading this article to reinvest, consider our article on Post-COVID credit requirements.

To be clear, there is a separate policy for homes with both foreclosure and bankruptcy. When this happens, the return to normal on your credit will take at least 7 years, but usually 10. Lenders consider bankruptcy to be a second negative credit event and treat you like you defaulted twice. It is often best to avoid bankruptcy at all costs.

Yes, we've written a number of helpful documents that will show you how to best apply for short sales. We made a guide for Carrington Mortgage Services that ranked very well, and considering their huge market share, it might be right for you.

What Can You Do for Me?

"I wish I'd called two months ago."

Talk to a Short Sale Attorney Today

We handle the lender negotiations. You focus on your next chapter. Free 30-minute consultation, flat-fee pricing.

All consultations are confidential.