What Just Changed, and Why It Matters to You

If you own investment properties through an LLC, partnership, corporation, or trust, and you sell without a traditional bank mortgage, the federal government now requires a detailed report filed with the Financial Crimes Enforcement Network (FinCEN).

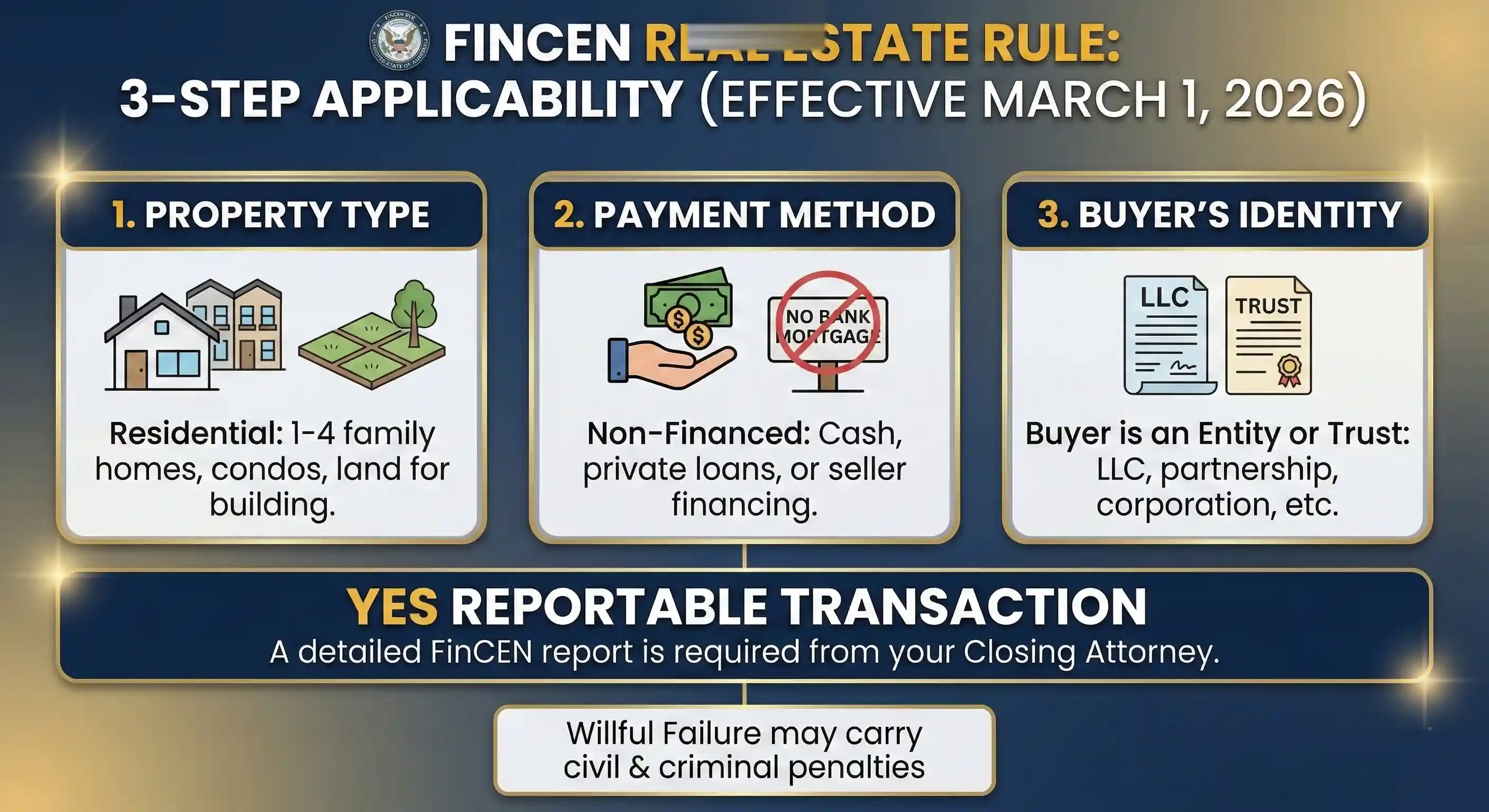

The rule is called the Residential Real Estate Rule, and it went into effect on March 1, 2026. It applies nationwide, to every transaction, regardless of the purchase price.

This is not a suggestion. It is a federal mandate under the Bank Secrecy Act. And it fundamentally changes how real estate closings work for investors.

Why this exists: The U.S. Treasury has identified all-cash and entity-based real estate purchases as a primary vehicle for money laundering. Previously, only certain high-value markets were monitored through Geographic Targeting Orders. Now every market, including all of Chicagoland, is covered. You can read the full rule and its rationale on FinCEN's official Residential Real Estate page.

Illicit actors often favor non-financed transfers of residential real estate to avoid scrutiny from financial institutions that have anti-money laundering program and Suspicious Activity Report filing requirements under the Bank Secrecy Act.U.S. Department of the Treasury, FinCEN Fact Sheet on the Residential Real Estate Rule

Is Your Transaction Covered?

A transaction triggers the reporting requirement when all three of these conditions are met:

- Residential property: Includes 1 to 4 family homes, condos, co-ops, townhouses, and even vacant land where the buyer intends to build residential units.

- Non-financed transfer: The purchase does not involve a mortgage from a regulated financial institution. This includes all-cash deals, seller financing, private lending, and any loan from a lender not subject to the Bank Secrecy Act.

- Buyer is an entity or trust: The transferee is an LLC, corporation, partnership, statutory trust, or any trust. Not an individual person.

If you are an investor who buys properties through an LLC (which is most of you), and the deal is financed privately or paid in cash, your transaction is reportable. If you are not sure whether you need an LLC in the first place, read our guide on setting up an LLC for rental property. And if you are financing that LLC purchase, here is what you need to know about LLC mortgages.

For sellers, this affects you too. While the reporting obligation technically falls on the closing professional, sellers involved in covered transactions will face new documentation requests, additional delays, and a longer paper trail. If your closing team is not prepared, your transaction could stall.

Exemptions: When a Transfer Is Not Reportable

Not every entity or trust purchase triggers a filing. FinCEN carved out a list of specific exemptions for lower-risk transfers. Some of the most common ones that apply to investors:

- Transfers to individuals. If the buyer is a natural person (not buying through an LLC, corp, or trust), no report is required.

- Bank-financed transactions. If a regulated financial institution provides the mortgage and is already subject to BSA/AML obligations, the transfer is generally exempt.

- Certain government and publicly traded entities. Transfers to federal, state, or local government agencies, securities reporting issuers, and certain regulated entities are excluded.

- Transfers through bankruptcy or court order. Certain judicially supervised transfers may qualify for exemption.

The full list of exemptions is longer and more specific than what we can cover here. FinCEN publishes the complete exemption details in their official FAQ, and we strongly recommend reviewing it if you think your deal might qualify. Do not assume you are exempt without confirming it first.

Trust Transfers: Different Rules for Beneficial Ownership

If the buyer is a trust rather than an LLC or corporation, the beneficial ownership rules work differently. For entities, FinCEN looks at individuals who hold 25% or more ownership or exercise substantial control. For trusts, the categories are more specific. FinCEN requires identification of:

- The trustee (or trustees) who manage the trust

- Each beneficiary of the trust

- Each grantor or settlor who established or funded the trust

- Any other individual with the authority to dispose of trust assets

If you hold property in a revocable living trust, an irrevocable trust, or a land trust, the person filing the report will need to identify every individual in those categories. Have those documents ready well before closing. If your trust structure is complicated, this is a conversation to have with your attorney now, not at the closing table.

Does This Apply to My Deal?

Answer three questions to find out if your transaction triggers FinCEN reporting.

1. Is the property residential (1 to 4 units, condo, co-op, or vacant land for residential building)?

2. Is the purchase non-financed (all cash, seller financing, private loan, or any lender not subject to BSA/AML)?

3. Is the buyer an LLC, corporation, partnership, trust, or other legal entity (not an individual person)?

What Gets Reported to the Federal Government

The Real Estate Report filed with FinCEN is not a simple form. It requires detailed identification of:

- The beneficial owners of the purchasing entity, meaning every individual who exercises substantial control or holds 25% or more ownership

- The entity's legal name, jurisdiction of formation, and identification numbers

- Transaction details including property address, sale price, and closing date

- The reporting person's own identification and role in the transaction

This information is filed through FinCEN's BSA E-Filing System and retained for five years. It is exempt from FOIA disclosure, so the public cannot see it. But law enforcement absolutely can. You can review the actual report form and filing instructions on the official FinCEN rule page.

Who Is Responsible for Filing? The "Reporting Cascade"

FinCEN created a seven-tier hierarchy called the reporting cascade to determine who files the report. The obligation falls on the professional who performs the highest function on the list. (The full breakdown, including edge cases like split settlements and designation agreements, is in the official FinCEN FAQ.)

- Closing or settlement agent listed on the closing statement ← Your IL Attorney

- Person who prepares the closing or settlement statement

- Person who files the deed with the recordation office

- Person who underwrites an owner's title insurance policy

- Person who issues an owner's title insurance policy

- Person who evaluates the status of the title

- Person who disburses the most funds

In Illinois, where attorneys handle closings, your closing attorney is almost always the reporting person. That means the attorney you choose determines whether your federal compliance is handled properly, or not. If you are not clear on what attorney review even involves, read that first. It will help you understand just how much your closing attorney actually does in a typical Illinois deal.

Penalty amounts are inflation-adjusted figures from the FinCEN FAQ under the Bank Secrecy Act. Willful violations can also result in criminal fines up to $250,000 and imprisonment up to five years.

What This Means for Chicago-Area Investors

If you are buying or selling investment properties in Cook, DuPage, Will, Kane, Lake, McHenry, Kendall, DeKalb, or Vermilion County through an LLC or trust, this rule applies to you right now.

Here is what is different about your closings starting today:

- More documentation upfront. Buyers must provide beneficial ownership information, government-issued IDs, and entity formation documents before closing can proceed.

- Longer timelines. The additional compliance steps mean closings require more lead time. If you are used to fast cash closings, build in extra days.

- Privacy implications. If you have used LLCs to maintain anonymity in your real estate holdings, that anonymity is significantly reduced. FinCEN now knows who is behind the entity.

- Criminal exposure for willful violations. This is not just civil penalties. Willful failure to comply can result in criminal liability under the Bank Secrecy Act.

And for investors who use creative financing structures like subject-to deals or wrap mortgages, the picture gets even more complicated. Those transactions often do not involve a regulated lender, which means they are almost certainly non-financed under this rule.

- Sign purchase contract

- Attorney review period

- Title search and clearance

- Closing and deed recording

- Funds disbursed, keys handed over

- Sign purchase contract

- Attorney review period

- Collect beneficial ownership docs and IDs from buyer entity

- Title search and clearance

- Determine reporting person via FinCEN cascade

- Closing and deed recording

- File Real Estate Report with FinCEN (within 30 days)

- Retain records for 5 years

- Funds disbursed, keys handed over

Don't Leave Your Next Closing to Chance

We are already filing FinCEN Real Estate Reports for our investor clients. If you have a deal closing soon, let's talk.

Why Your Closing Attorney Matters More Than Ever

Before this rule, a closing was a closing. You needed an attorney to review the contract, handle title, and make sure the deed got recorded. Standard stuff.

Now, your closing attorney is also your federal compliance officer for the transaction. They are the one filing reports with a division of the U.S. Treasury. They are the one who needs to verify beneficial ownership. They are the one carrying the liability if the filing is wrong, late, or missing.

This is not something you want handled by the cheapest option you can find on Google.

What to ask your closing attorney

- Are you registered with FinCEN's BSA E-Filing System?

- Do you have a process for collecting beneficial ownership information?

- Have you updated your closing workflow for the new rule?

- Will you handle the filing, or are you outsourcing it to a third party?

If they hesitate on any of those questions, that is your answer.

"Working with Justin was like working with a great friend. His knowledge and experience is extensive and he's able to explain complex issues in simple understandable terms. Justin has a knack for creativity and out of the box thinking that helped place me in the best possible situation. I cannot recommend Justin enough. The value he offers far exceeds Justin's already reasonable fees."

Is Your Current Attorney Ready for FinCEN Compliance?

If any of this sounds familiar, your closing is at risk:

- Your attorney has not mentioned the new FinCEN reporting rules

- They cannot tell you what a "reporting cascade" is

- They have never filed a Real Estate Report through the BSA E-Filing System

- They have not asked for your LLC's beneficial ownership documentation

- They quoted the same timeline and process as last year with no changes

No pressure. We will tell you exactly what your current deal needs, even if you do not hire us.

"Attorneys are a dime a dozen; however, Justin Abdilla is hungry, driven, and committed to serving his clients in the best possible way. I have personally hired Justin for personal real estate transactions, and referred much real estate sales business. I like that Justin is attentive, isn't afraid to pick up the phone to communicate, and help to solve solutions, rather than adding to the problems."

How to Prepare Your Next Transaction

Whether you are selling or buying, here is what you should do now:

- Gather your entity documents. Have your Articles of Organization, Operating Agreement, and EIN confirmation ready. If you are a trust, have the trust agreement and schedule of beneficiaries. Not sure what you need? Our LLC for rental property guide walks through all of it.

- Identify your beneficial owners. Know who holds 25% or more ownership and who exercises substantial control. Have their government-issued photo IDs ready.

- Coordinate with your attorney early. Do not wait until a week before closing. The new compliance requirements need lead time.

- Review your holding structure. If privacy was a key reason for using an LLC, understand that the calculus has changed. You may want to discuss restructuring options with a due diligence attorney.

And if you are considering selling a property as-is or doing a 1031 exchange into your next investment, the FinCEN reporting layer makes it even more important to have a single attorney quarterbacking the whole thing. You do not want three different professionals pointing fingers about who was supposed to file.

Already in contract? If your deal is closing this month, call us now. We can get your FinCEN compliance sorted before your closing date, but we need time to do it right.

"Justin was our attorney selling a property. He was very responsive and answered every question we had. He reviewed so many documents and had great feedback and suggestions. We had a special situation and his suggestion saved us enough money to buy a used car."

The Bottom Line

The FinCEN Residential Real Estate Rule is the biggest regulatory change to hit real estate investors in years. It does not matter whether your deal is a $150,000 rental in Berwyn or a $2 million portfolio sale in DuPage County. If an entity or trust is involved and there is no bank mortgage, the federal government wants a report.

This is the new reality. The investors who adapt quickly, and hire attorneys who are already prepared, will keep their closings on track. The ones who don't will face delays, penalties, and unnecessary risk.

At Abdilla & Associates, we have been representing landlords and real estate investors across Chicagoland for over a decade. We have already integrated FinCEN's reporting requirements into our closing process. Our Super Lawyers Rising Stars recognition (2021 to 2026) and 70+ five-star reviews are not just numbers. They reflect hundreds of investor transactions handled the right way.

If you have a transaction coming up, book a free consult. We will walk you through exactly what you need.

Official FinCEN Resources: We encourage every investor to review the primary source material directly. Here are the pages you should bookmark:

- FinCEN Residential Real Estate Rule (main rule page with quick reference guides and filing resources)

- FinCEN RRE Frequently Asked Questions (the most detailed breakdown of every requirement, exemption, and edge case)

- BSA E-Filing System (where reports are actually filed)