Table of Contents

How Much Do You Lose Selling a House As Is in Illinois?

Selling a house as is typically means accepting 5% to 30% less than market value, depending on the property’s condition, where it’s located, and who’s buying it. A home that needs cosmetic work might sell for 5% to 10% below comparable move-in-ready properties. A house with foundation issues, a failing roof, or outdated electrical could take a 20% to 30% haircut.

Those are the national averages. In Illinois, the math gets more specific because of how our closing process works, what you’re required to disclose, and the role your attorney plays in protecting you from post-sale liability. I’ve represented sellers on both sides of this decision, and the gap between a smart as-is sale and a costly one usually comes down to preparation and pricing strategy, not whether you made repairs.

If you’re trying to figure out whether selling as is makes sense for your situation, this guide breaks down the real numbers, the legal requirements in Illinois, and the scenarios where selling as is actually puts more money in your pocket than spending $30,000 on renovations that only add $15,000 in sale price.

How Much Less Will You Get Selling a Home As Is?

The discount buyers expect on an as-is property depends on three things: the condition of the home, the type of buyer, and whether the property can qualify for conventional financing.

That last row is critical. If your home is in a condition where a lender won’t approve a mortgage on it, think an unsafe electrical panel, a roof beyond its useful life, or active water intrusion, you’ve eliminated every buyer who needs a loan. That shrinks your buyer pool to cash investors, and cash investors price accordingly.

On a $330,000 home in DuPage County, a 15% as-is discount means you’re looking at roughly $280,500 instead of $330,000. That’s a $49,500 reduction. Whether that number makes sense depends on what it would cost to bring the property to market-ready condition and how long those repairs would take.

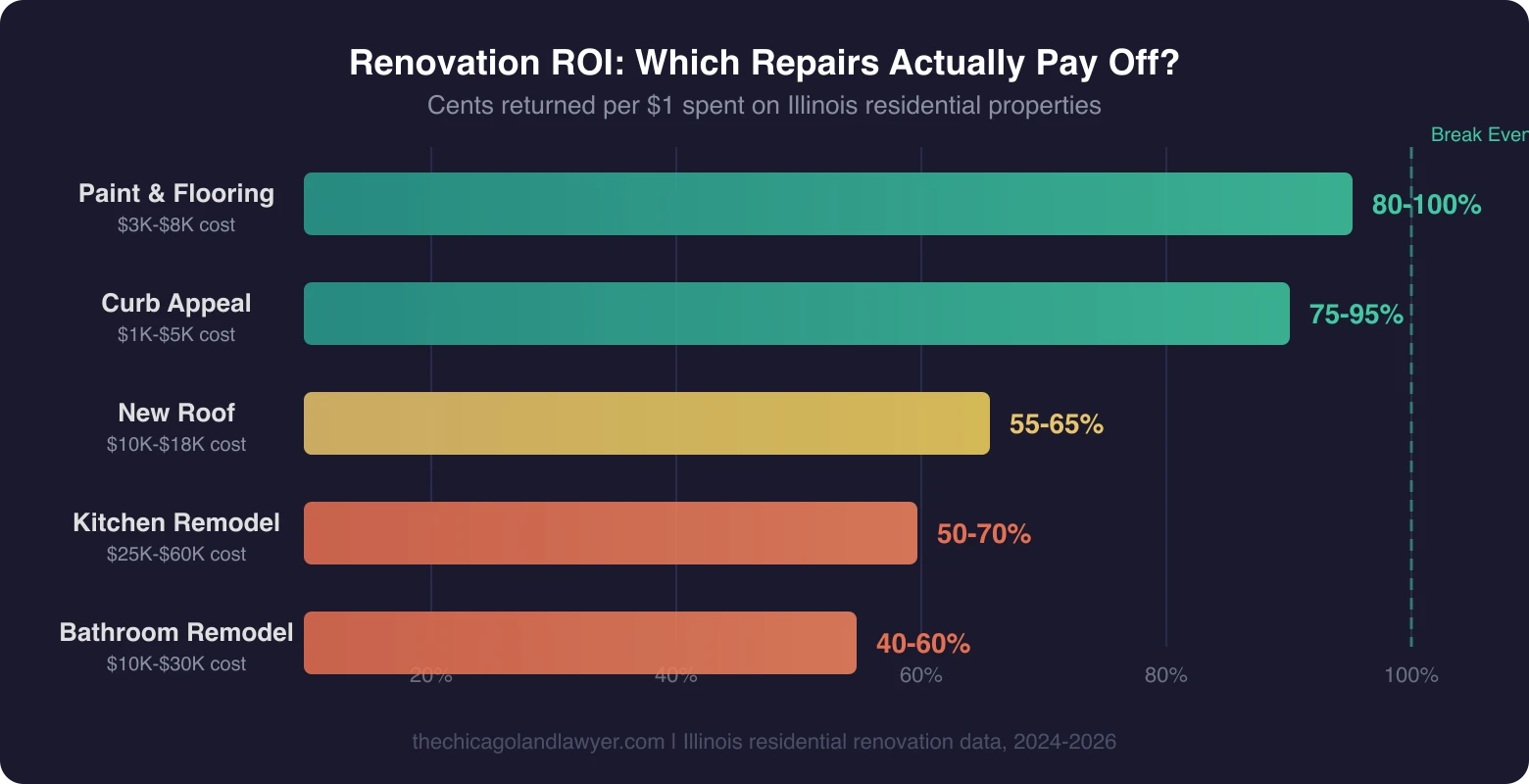

The Repair Math That Most Sellers Get Wrong

Sellers tend to compare the as-is discount against the cost of repairs. That’s only half the equation. You also need to account for carrying costs during the repair period: mortgage payments, property taxes, insurance, and utilities. If a $25,000 renovation takes three months, add another $5,000 to $8,000 in holding costs on top of the contractor’s bill.

Then there’s the return on investment problem. Not every dollar you spend on repairs comes back at closing. Kitchen remodels in Illinois return roughly 50% to 70% of cost. A new roof returns closer to 60%. Cosmetic updates like paint and flooring are the best bang for the buck at 80% to 100% return, but they don’t fix the structural issues that drive the biggest discounts.

What Does Selling a House As Is Actually Mean?

Selling as is means you’re telling buyers that you won’t make repairs or provide credits for property defects. The buyer accepts the home in its current condition. You’re not hiding anything, and you’re not promising anything beyond what’s there.

In Illinois, an as-is sale is typically handled through a modified version of the Multi-Board Residential Real Estate Contract, with specific as-is language in the contract rider. The contract makes clear that the seller is not obligated to perform any repairs, even if the home inspection reveals issues. If you want to see how the contract actually works, I walk through it in the video below.

A lot of sellers misunderstand this part: as-is does not mean as-unknown. You still have disclosure obligations, and in Illinois, those obligations have teeth.

Illinois Disclosure Requirements for As-Is Sales

Illinois sellers are required to complete the Residential Real Property Disclosure Report regardless of whether the sale is as-is. This is a statutory requirement under the Illinois Residential Real Property Disclosure Act (765 ILCS 77), and selling “as is” does not give you a pass.

The disclosure form covers known defects in:

- Foundation and structural components

- Roof age and condition

- Plumbing, electrical, and HVAC systems

- Water intrusion, flooding, or drainage issues

- Environmental hazards (lead paint, asbestos, radon, mold)

- Boundary disputes or encroachments

- Code violations or zoning non-compliance

If you know about a problem and don’t disclose it, selling as is won’t protect you. A buyer who discovers undisclosed defects after closing can sue for fraud or violation of the disclosure act. I’ve seen these cases, and they’re expensive to defend even when the seller eventually wins.

For a full breakdown of what Illinois requires, read our complete disclosure guide.

If you’re unsure whether your disclosures are complete or how to protect yourself in an as-is transaction, that’s exactly what a 15-minute consultation covers. Call (630) 839-9195 or book a time online.

Why Attorney Review Matters More in As-Is Sales

In Illinois, the attorney review period gives both sides five business days to modify or cancel the contract after signing. In a standard sale, attorney review is where you negotiate inspection items and repair credits. In an as-is sale, attorney review becomes your primary protection against future liability.

Your attorney’s job in an as-is sale is to make sure the as-is language in the contract is airtight, that your disclosures are complete and accurate, and that the contract doesn’t contain provisions that could expose you to claims later. Buyers’ attorneys will try to carve out exceptions to the as-is terms during review. Without your own attorney reviewing those modifications, you might agree to terms that undermine the entire point of selling as is.

This is where the competitors’ advice breaks down. Some national real estate sites will tell you an attorney isn’t required for an Illinois real estate transaction. That’s technically true, and it’s terrible advice. Illinois is one of a handful of states where attorney involvement in residential transactions is standard practice, and in an as-is sale, the legal risk is higher, not lower. A flat-fee real estate attorney will cost you a fraction of what a post-sale lawsuit costs. See our full list of real estate legal services for what we cover.

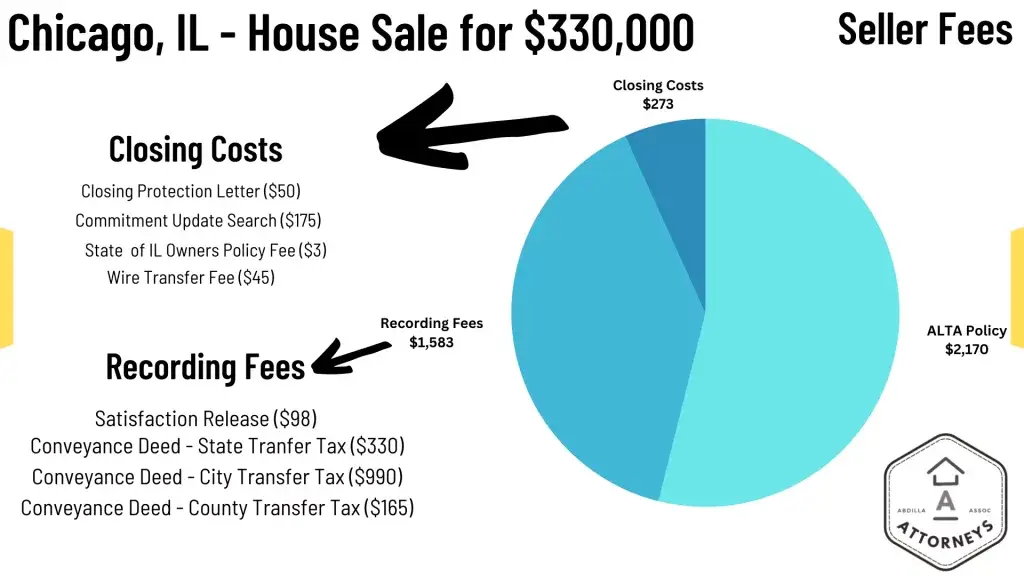

Closing Costs When You Sell Your House As Is in Illinois

Selling as is doesn’t change your closing costs. Whether you sell as-is or after $50,000 in renovations, these costs are the same. Below is a realistic breakdown on a $330,000 sale in the Chicago suburbs:

Seller Closing Costs

| Fee | Amount |

|---|---|

| Title insurance (ALTA Owner’s Policy) | ~$2,170 |

| State of Illinois transfer tax (0.10%) | $330 |

| County transfer tax (0.05%) | $165 |

| Municipal transfer stamps (varies by city) | $0 – $1,650 |

| Recording fees | $15 – $50 |

| Wire transfer fee | $45 |

| Closing protection letter | $25 – $50 |

| Prorated property taxes | Varies |

| Attorney fee (flat fee) | $500 – $1,000 |

| Typical Total Seller Closing Costs | $3,250 – $5,460 |

Plus prorated property taxes. Based on a $330,000 sale in suburban Cook/DuPage County.

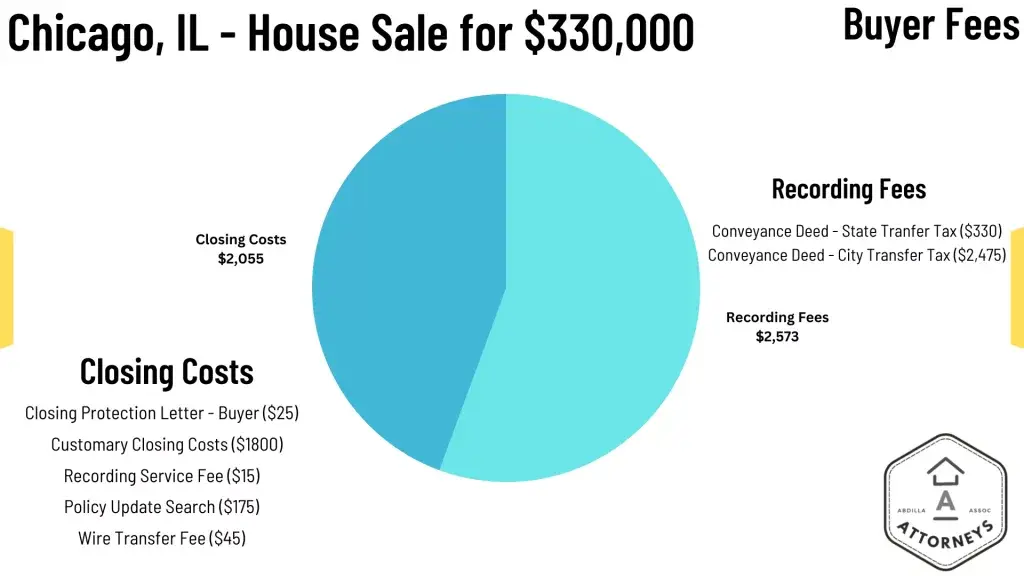

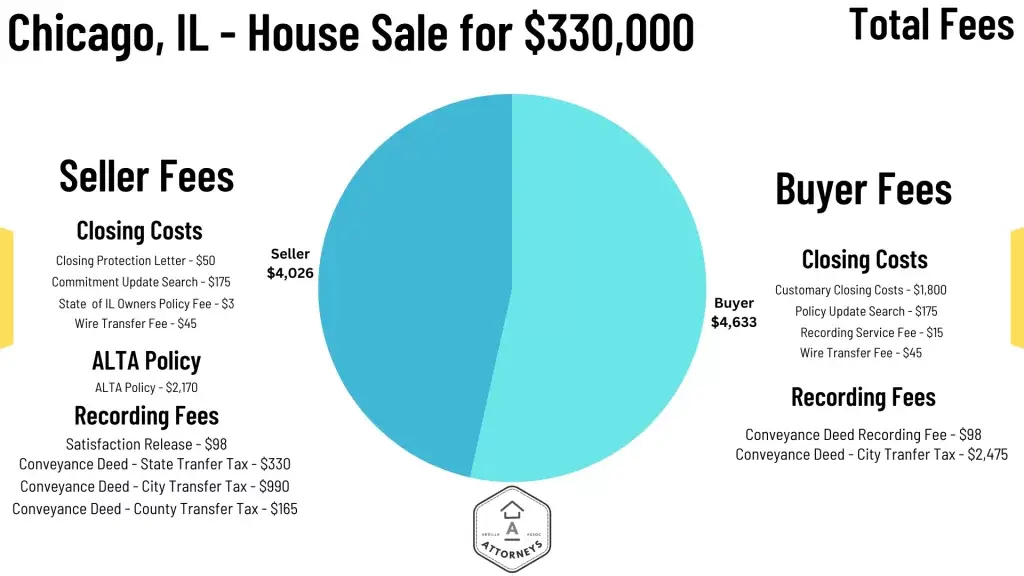

If you’re working with a real estate agent, add 5% to 6% commission on top of that, which is $16,500 to $19,800 on a $330,000 sale. If you’re selling FSBO, you eliminate that cost but still typically offer a 2.5% to 3% buyer’s agent commission. On the buyer’s side, closing costs break down differently but still add up fast.

Combined, the total closing costs on both sides of a $330,000 transaction look like this:

What You Won’t Save by Selling As Is

Some sellers assume that an as-is sale means lower closing costs. It doesn’t. Title insurance, transfer taxes, and attorney fees are the same regardless. What you save is the cost of repairs and the time they take. What you lose is the price difference between your as-is sale price and what you could have gotten after making improvements. That trade-off is the entire decision.

When Selling a Home As Is Makes Financial Sense

Selling as is isn’t always a loss. There are situations where it’s the financially smart move.

Inherited properties are the clearest case. If you’ve never lived in the home, you may not know its full condition, and representing that repairs have addressed all issues is a liability risk. Selling as is with complete disclosures (to the extent of your knowledge) is cleaner and legally safer. Illinois disclosure obligations are lessened when the seller hasn’t occupied the property, though you still must disclose what you know.

The math also favors as-is when repair costs exceed the potential return. If a home needs $60,000 in work but the repairs would only increase the sale price by $30,000 to $40,000, you’re losing money by renovating. This is common with older homes in areas where comparable properties are also dated, so buyers aren’t expecting updated finishes anyway.

Speed matters too. Renovations take time, and time costs money. If you’re carrying two mortgages, relocating for work, or dealing with a divorce or estate settlement, the speed of an as-is sale (especially to a cash buyer who can close in 14 to 21 days) may be worth the price discount. In a seller’s market with low inventory, the discount might only be 5% to 8% because buyers are willing to overlook condition issues just to get into a home.

And if you’re facing foreclosure, selling as is at a discount is almost always better than the alternative on your credit report. If you’re underwater on your mortgage, a short sale may be an option worth exploring with your attorney.

When You Should Make Repairs Instead

If the issues are purely cosmetic, spending money almost always makes more sense than taking the as-is discount. Fresh paint, new carpet, updated light fixtures, and professional staging cost $3,000 to $8,000 and typically recover $5,000 to $15,000 in sale price. Buyers respond disproportionately to how a home looks in listing photos.

The single most impactful fix is financing eligibility. If a lender’s appraiser will flag issues that prevent loan approval, things like peeling paint on a pre-1978 home, missing handrails, or a non-functional furnace, fixing those specific items opens your buyer pool from cash-only to everyone. That single change can swing your sale price by 15% to 20%.

Market conditions matter, too. When inventory is high and buyers have options, an as-is listing sits longer and attracts lowball offers. Targeted repairs and proper staging help your home compete in a soft market. And sometimes the discount buyers demand for “as-is” far exceeds the cost of fixing one specific issue. If the roof needs replacing and buyers are discounting $30,000 but a new roof costs $12,000, that’s an $18,000 reason to pick up the phone and call a roofer.

How to Sell a Home As Is and Minimize Your Loss

If you’ve decided that selling as is is the right call, the goal is to leave the least amount of money on the table. Every one of these steps costs less than skipping it.

Start with a pre-listing inspection. It sounds counterintuitive when you’re selling as-is, but knowing exactly what’s wrong lets you price accurately, disclose fully, and avoid surprises that blow up deals mid-transaction. A $400 inspection prevents a $15,000 renegotiation.

Pricing is the next critical piece. Overpricing an as-is home is the most expensive mistake sellers make. The property sits, accumulates days on market, and then you end up accepting less than you would have if you’d priced competitively at the start. Work with a local agent or appraiser who understands as-is valuations in your area.

List on the open market rather than going straight to a cash-offer company. Cash buyers and iBuyers typically pay 70% to 85% of after-repair value. Listing on the MLS, even as-is, exposes the property to investors, flippers, handy first-time buyers, and bargain hunters. Competition drives the price up. You don’t need to renovate, but you do need to present the home at its best current condition. Professional photos of a clean, decluttered as-is home outperform phone photos of a cluttered one every time.

Finally, get a real estate attorney involved early. In an as-is sale, your attorney drafts the as-is rider, reviews buyer counter-proposals during attorney review, ensures your disclosures are complete, and protects you from post-closing claims. Our real estate services cover everything from contract to closing at a flat fee.

Frequently Asked Questions About Selling As Is

How much do you lose selling a house as is?

Most sellers lose 5% to 30% compared to market value. Homes with only cosmetic issues typically sell for 5% to 10% less. Properties with major structural problems or that can’t qualify for financing may sell for 20% to 30% less. The exact discount depends on your local market, the property’s condition, and the buyer pool.

Do I still have to disclose defects if I sell as is in Illinois?

Yes. Illinois law requires sellers to complete the Residential Real Property Disclosure Report regardless of whether the sale is as-is. You must disclose all known material defects. Failure to disclose can result in lawsuits for fraud or violation of the Illinois Residential Real Property Disclosure Act.

Can I sell my house as is if I have a mortgage?

Yes. You’ll pay off your remaining mortgage balance from the sale proceeds at closing. If your mortgage balance exceeds the as-is sale price, you’re looking at a short sale, which requires your lender’s approval. Some investors will also offer subject-to financing, where they take over your existing mortgage payments. That can work in certain situations, but the legal risks are significant and you need an attorney reviewing the terms. Talk to an attorney about your options before listing.

Do I need a real estate attorney to sell as is in Illinois?

Technically, no. Practically, absolutely. Illinois is an attorney-review state, and in an as-is transaction, the contract language protecting you from future liability needs to be precise. An experienced real estate attorney also ensures your disclosures are complete and that buyer’s attorney modifications during the review period don’t create exposure for you.

Will banks finance a house sold as is?

It depends on the property’s condition. If the home meets minimum habitability standards (functioning HVAC, intact roof, safe electrical, no active water damage), buyers can typically get conventional or FHA financing. If the home fails these standards, you’re limited to cash buyers or buyers using renovation loans like FHA 203(k), which are slower to close and more complex.

Is selling as is the same as selling to an investor?

No. You can sell as-is to any buyer, including first-time homebuyers, DIY enthusiasts, and traditional buyers. Listing on the MLS as-is opens you to the entire market. Selling directly to an investor or cash-offer company is one option, but it typically results in a lower sale price than open-market competition.

What’s the difference between selling as is and selling FSBO?

These are separate decisions. As-is means you won’t make repairs. FSBO (For Sale By Owner) means you won’t use a listing agent. You can sell as-is with an agent, as-is FSBO, or make repairs and sell FSBO. The two choices are independent, though combining them (as-is + FSBO) requires careful attention to contract language and disclosures.

How long does it take to sell a house as is?

As-is homes listed on the MLS typically sell within the same timeframe as comparable properties in the same area, though they may sit slightly longer if overpriced. Cash sales to investors can close in 14 to 21 days. A traditional as-is sale through the MLS with a financed buyer typically takes 35 to 45 days from contract to closing.

Managing Attorney, Abdilla and Associates

Justin Abdilla is a practicing Illinois real estate attorney who handles residential closings, as-is sales, FSBO transactions, and investor deals across Chicagoland. He is licensed by the Illinois ARDC and serves clients in Cook, DuPage, Will, Kane, and Lake counties.